BMO mortgage rates are drawing serious attention from home-buyers in 2025. As interest rates recently begin to stabilize, BMO offers a range of terms that balance flexibility, affordability, and long-term planning. Understanding BMO’s mortgage options can give you a clear financial edge.

With many key features designed for today’s buyers, the bank caters to a broad range of borrower needs. In this guide, we’ll explore the latest BMO mortgage rates, highlight the best terms for 2025. Additionally, we also share practical tips to help you make informed decisions.

Overview of BMO Financial Corp.

Founded in 1817, BMO Financial Corp. is one of the most established and trusted banks in North America. With over $1.4 trillion in total assets, BMO serves more than 13 million customers across different select global markets.

It operates through different core business segments: Personal, Business and Commercial Banking, Wealth Management, Global Asset Management and BMO Capital Markets. This structure allows BMO to offer a full range of services from everyday banking to investment advisory and institutional financing.

At BMO, the focus is on building, investing, and transforming the way the organization operates to consistently drive stronger performance. In particular, this performance means to generate greater value for customers, clients, and communities. BMO is committed to helping individuals make real financial progress, while also supporting business clients as they pursue growth and innovation.

At the same time, the bank invests in the future-readiness of its workforce. As a result, employees tend to adapt and lead in an evolving financial landscape. Through these efforts, BMO actively contributes to a thriving economy, a more sustainable future, and a truly inclusive society.

For home-buyers considering BMO mortgage rates, this combination of scale, stability, and customer-focused service makes the bank a competitive and reliable lender in 2025.

General Explanation to BMO Mortgage Rates

A mortgage is a type of loan provided by a financial institution like BMO. It helps individuals purchase or refinance a home. When you take out a mortgage, you agree to repay the loan amount over a defined period through regular payments. These payments typically include both the principal (the amount borrowed) and interest, along with any applicable fees. The exact terms, such as the repayment period and interest rate, are agreed upon between the borrower and the lender at the time of application.

The mortgage rate refers to the interest charged on this loan and plays a critical role in determining how much you’ll pay over time. Mortgage rates are not static but they fluctuate based on broader economic conditions, especially the benchmark interest rates set by the U.S. Federal Reserve. When interest rates rise, mortgage rates often increase, making borrowing more expensive. Conversely, falling interest rates can create favorable conditions for locking in a lower mortgage rate.

BMO mortgage rates follow the same principle. They are tied closely to economic trends and benchmark rates but may also reflect BMO’s internal lending strategy, customer relationship incentives, and promotional programs. BMO offers both fixed and variable mortgage rates with various term lengths to suit different financial goals. Whether you’re buying your first home or refinancing an existing loan, it’s necessary to understand how BMO mortgage rates work. As a result, you can make informed, cost-effective decisions.

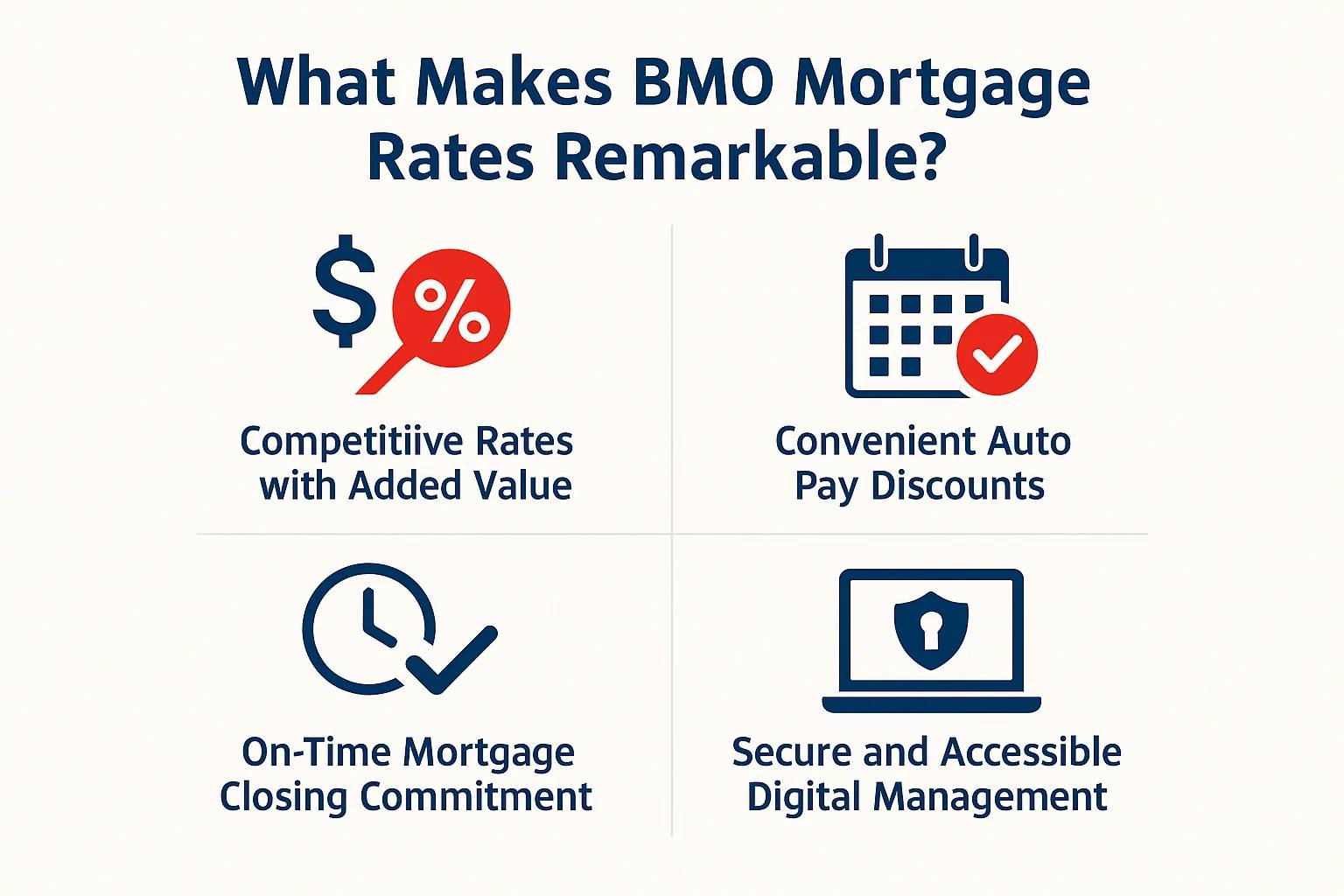

What Makes BMO Mortgage Rates Remarkable?

Nowadays, competitive rates alone are no longer enough. Today’s homebuyers expect a more complete experience combining financial value with convenience, reliability, and digital accessibility. That’s why BMO mortgage rates stand out.

Competitive BMO Mortgage Rates with Added Value

BMO mortgage rates don’t just align with national averages. However, it adds real value through cost-saving opportunities. Homebuyers can save up to $500 in closing costs, which can make a significant difference when managing upfront expenses.

Additionally, existing BMO customers benefit from special relationship pricing, allowing them to unlock even lower rates simply by maintaining an account with the bank. These financial perks are particularly appealing in a market where affordability matters more than ever. By combining attractive base rates with these incentives, BMO provides not only a loan but also a strategic advantage for cost-conscious buyers.

Convenient Auto Pay Discounts

One of the standout features of BMO mortgage rates is the convenience along with savings enabled through Auto Pay. When customers set up automatic payments from a BMO checking account, they receive a 0.125% discount on their mortgage rate. This may seem small at first glance. However, over the lifetime of a mortgage, it can amount to thousands of dollars in interest savings.

Beyond the financial benefits, Auto Pay also reduces the risk of missed payments. Therefore, it’s easier for homeownership to manage. It’s a simple step with powerful results, reinforcing BMO’s focus on creating smarter financial habits for its clients.

On-Time Mortgage Closing Commitment

Timeliness is critical during the home-buying process, and BMO addresses this head-on with its On-Time Mortgage Closing Commitment. This promise ensures that if your mortgage doesn’t close on schedule, you may be eligible for up to $5,000 back in closing costs. It’s a bold guarantee that reflects BMO’s operational confidence and dedication to customer satisfaction.

Delays during closing can be stressful and costly. However, BMO’s policy mitigates that risk and provides buyers with added peace of mind. This feature not only highlights the bank’s efficiency but also sets a strong standard for reliability in an industry where delays are all too common.

Secure and Accessible Digital Management

In today’s digital-first world, flexibility and access are just as important as rates and terms. BMO ensures that customers can easily manage BMO mortgage rates through its Online Banking and Mobile Banking platforms. Whether it’s reviewing payment schedules, checking balances, or making additional payments, everything can be done on the go.

This seamless integration allows borrowers to stay on top of their finances without visiting a branch so it’s both convenience and security. Consequently, it’s ideal for busy professionals, first-time buyers, or anyone who values real-time access to their mortgage account. With these tools, BMO empowers customers to take full control of their home loan journey anytime, anywhere.

Different Options of BMO Mortgage Rates

There are a variety of BMO mortgage rates tailored to fit different financial strategies and timelines.

Fixed BMO Mortgage Rate

A fixed mortgage rate means your interest rate remains unchanged for the entire duration of your loan term. From the moment you close on your mortgage to the day you make your final payment, your interest rate stays exactly the same unless you choose to refinance. This consistency results in predictable monthly principal and interest payments. Therefore, it’s easier to budget your finances year after year. That’s why fixed-rate mortgages are considered a reliable and steady choice for long-term financial planning.

BMO fixed mortgage rate comes with several features designed to enhance this stability and align with a wide range of homeownership goals. Moreover, BMO also offers flexibility in terms, allowing borrowers to choose from various fixed-rate durations that suit their plans.

Regardless of your purpose and terms, BMO allows you to secure a fixed rate across different property types. By locking in a rate, homeowners can guard against future market volatility and maintain control over one of their most important monthly expenses. That reliability is especially helpful for buyers who plan to stay in their home for many years and want to avoid surprises.

To make repayment even simpler, BMO supports Auto Pay through its checking accounts, giving you peace of mind and the added benefit of a rate discount in some cases.

Adjustable BMO Mortgage Rate

An adjustable mortgage rate starts with a fixed interest rate for a predetermined period, typically between three and ten years. During this initial phase, your monthly principal and interest payments remain steady, allowing for short-term budgeting stability. However, once the fixed-rate period ends, the loan shifts to a variable interest rate. This rate adjusts periodically based on an external financial benchmark which is determined by neutral third party and reflects real-time market conditions.

One of the main advantages of this type of BMO mortgage rate is lower payments early on. Because lenders assume the risk of rising rates later, they typically offer a lower introductory rate than comparable fixed rate. This can result in significant short-term savings. Therefore, this rate is particularly appealing to buyers who expect to refinance, relocate, or sell the home before the adjustment period kicks in. After the fixed period, your interest rate may adjust semi-annually or annually, depending on your loan terms. Accordingly, your monthly payments will rise or fall.

BMO’s adjustable mortgage rates are also structured with protective caps in place. These limits control how much your interest rate can increase during a single adjustment and over the life of your loan. While your BMO mortgage rate can fluctuate based on the market, these caps ensure you’re shielded from extreme spikes in payment amounts. Moreover, when the principal and interest portions of your payment can vary, your escrow payments covering property taxes, insurance, and other obligations, may also change over time based on local cost adjustments.

In addition, BMO makes ARMs more manageable with convenient features like Auto Pay from a BMO checking account. This setup not only streamlines your monthly payments but can also help you qualify for additional rate discounts. For borrowers who are balancing homeownership with responsibilities like payday loans or other short-term credit needs, these features offer welcome flexibility. Altogether, BMO’s adjustable mortgage rates combine short-term affordability with long-term adaptability.

Low Down Payment BMO Mortgage Rate

Low down payment mortgage rates refer to a type of BMO mortgage rate allowing borrower contributes a smaller-than-usual down payment. Their contribution is often less than 20% of the home’s purchase price.

While low down payment mortgages make homeownership more accessible, the interest rate may differ slightly from those available to borrowers with larger down payments. That’s because a lower down payment typically means higher risk for BMO, which can be reflected in the pricing of BMO mortgage rate.

When borrowers qualify for low down payment mortgage programs, the interest rate offered is often structured through federally backed or specially designed products. Here are some common types you might find through BMO Financial Corp.:

Neighborhood Home Loan Product

This program typically supports borrowers purchasing in specific geographic areas or low-to-moderate income neighborhoods. It may offer below-market mortgage rates and reduced down payment requirements. BMO may also waive certain fees or offer special fixed-rate terms to enhance affordability.

FHA Loans

Backed by the Federal Housing Administration, FHA loans are among the most popular low down payment options, allowing you to put down as little as 3.5%. Rates for FHA loans are often competitive but can vary based on credit score and required mortgage insurance premiums (MIP). While the base rate might be slightly higher than conventional loans, the government backing makes these loans widely accessible, especially for first-time buyers.

Home Possible (by Freddie Mac)

This program offers low fixed mortgage rates for borrowers with limited income and a down payment as low as 3%. Home Possible also allows flexible income sources, which helps more borrowers qualify. BMO provides rate incentives for Home Possible participants who use automatic payments or meet certain income thresholds.

Housing Finance Agency (HFA) Program

HFA loans are state-run programs that often include interest rate reductions, down payment assistance, or grants. These rates are typically lower than market average, and terms vary depending on the state. BMO partners with local agencies to extend these offers to eligible borrowers.

Veterans Affairs (VA) Loans

VA loans are available to eligible U.S. military service members, veterans, and certain family members. These loans require no down payment and often feature some of the lowest mortgage rates available, thanks to VA backing. There’s no private mortgage insurance (PMI) required, which makes the effective rate even more affordable.

Consequently, it’s an attractive option for borrowers who want to preserve savings for other goals such as: growing a personal investment portfolio, or simply reducing monthly debt tied to credit cards.

Jumbo BMO Mortgage Rate

A jumbo mortgage loan is designed for borrowers who need to finance a home that exceeds the limits of a standard conforming loan. At BMO, that threshold starts at $806,500. If you’re buying a high-value property or looking to upgrade into a luxury home, a jumbo loan may be necessary to cover the larger purchase amount. Since these loans involve higher risk and larger borrowing amounts, they often come with specialized terms and that includes jumbo mortgage rates.

With a jumbo mortgage, borrowers can choose from both fixed and adjustable BMO mortgage rate options, providing flexibility based on your financial goals. Moreover, one standout advantage of BMO’s jumbo mortgage rate is its competitive structure, often combined with low closing costs and favorable financing terms.

For qualified buyers, BMO offers up to 89.99% loan-to-value (LTV). This means you may only need a 10%–11% down payment to secure your loan. Importantly, BMO’s jumbo loans do not require private mortgage insurance (PMI) – a major cost-saver that can improve your effective borrowing rate over time.

Moreover, you can lock in your BMO mortgage rate for a longer period before closing due to extended rate lock program. As a result, you can avoid potential market shifts during the underwriting process.

BMO Mortgage Rates Updated 2025

BMO mortgage rates continue to reflect a balanced approach between competitiveness and stability. Whether you’re a first-time homebuyer, refinancing your existing loan, or investing in property, BMO offers a variety of rate structures to fit different financial needs. Moreover, each updated to align with current market conditions.

Fixed Mortgage Rate

Fixed mortgage rates at BMO continue to offer stability for borrowers looking for predictable payments. While average fixed mortgage rates currently range between 5.20% and 5.49%, the exact rate you receive will depend on several personal and loan-specific factors.

Your final fixed rate can vary based on:

-

The purchase price of your home

-

The size of your down payment

-

Your loan term length (e.g., 15, 20, or 30 years)

-

Your credit profile and any discounts (like Auto Pay or relationship pricing)

To better understand what your fixed mortgage payments might look like, you can use BMO’s Fixed Rate Mortgage Calculator. Simply input necessary information.

For example, you’re buying a home priced at $260,000 and plan to put down 20% (or $52,000). You choose a 4-year term at a fixed interest rate of 5.20%.

| Input Details | Value |

|---|---|

| Purchase Price | $260,000 |

| Down Payment (20%) | $52,000 |

| Loan Amount | $208,000 |

| Term Length | 4 years |

| Fixed Interest Rate | 5.20% |

| Payment Components | Amount (Monthly) |

|---|---|

| Principal & Interest | $4,809 |

| Taxes & Insurance | $354 |

| Total Monthly Payment | $5,163 |

As shown in the calculator preview, the majority of your payment goes toward principal and interest, with a smaller portion covering taxes and insurance. Whether you’re planning for a short-term commitment or a long-term home, BMO’s fixed mortgage solutions in 2025 offer clarity and control in a fluctuating rate environment.

Adjustable Mortgage Rate

The actual adjustable mortgage rate you receive depends on a variety of factors. These include the initial interest rate offered by BMO, the index rate, and the margin. Additionally, the loan term, how often the rate adjusts, and your personal financial profile play a role in determining your final rate. For example, someone managing multiple financial obligations like personal loans might receive different terms than someone with a simpler financial profile.

To better understand what your monthly payments could look like, you can use BMO’s Adjustable Rate Mortgage Calculator.

For instance, let’s say you’re purchasing a $260,000 home with a 20% down payment and choose an ARM with a 3.75% initial interest rate, fixed for the first 6 months. Based on BMO’s calculator, your estimated monthly payment would be around $5,027, including $4,673 in principal and interest, plus $354 for property taxes and insurance. After the fixed period, the rate may adjust every 6 months, with a maximum increase of 1.00% per adjustment and a lifetime cap of 7.50%.

| Details | Value |

|---|---|

| Home Purchase Price | $260,000 |

| Down Payment (20%) | $52,000 |

| Loan Amount | $208,000 |

| Initial Interest Rate | 3.75% |

| Initial Fixed Period | 6 months |

| Loan Term | 4 years |

| Estimated Monthly Payment | $5,027 |

| → Principal & Interest | $4,673 |

| → Taxes & Insurance | $354 |

| Adjustment Frequency | Every 6 months |

| Max Rate Increase (per adj.) | 1.00% |

| Lifetime Rate Cap | 7.50% |

| Margin | 2.75% |

| Index Rate | 1.25% |

Low Down Payment Mortgage Rate

If you’re planning to buy a home with a limited down payment, several BMO mortgage rate programs designed to help you qualify with less cash upfront.

| Program | Min. Down Payment | Credit Score | Mortgage Insurance | Rate Characteristics | Down Payment Assistance |

|---|---|---|---|---|---|

| Neighborhood Home Loan | As little as 1% | 640 | No | Among the lowest monthly payments, below market | $16,000 or more |

| FHA Loans | As little as no funds | 580 | Yes | Standard fixed rate, may be slightly higher due to MIP | $16,000 or more |

| Home Possible | As little as no funds | 620 | Yes | Low fixed rates for qualified borrowers | $16,000 or more |

| Housing Finance Agency (HFA) | As little as 1% | 640 | Yes | Slightly higher rates, most assistance available | $16,000 or more |

| Veterans Affairs (VA) | As little as no funds | 580 | No | Some of the lowest fixed rates available | $16,000 or more |

For borrowers looking to refinance an existing mortgage, BMO also provides flexible low down payment options that come with competitive rates and closing cost assistance.

| Program | Max. LTV | Credit Score | Mortgage Insurance | Rate Characteristics | Closing Cost Assistance |

|---|---|---|---|---|---|

| Neighborhood Home Loan | Up to 97% | 640 | No | Lower fixed rates, flexible terms | $2,000 or more |

| FHA Loans | Up to 96.5% | 580 | Yes | Standard fixed rate with MIP | $2,000 or more |

| Home Possible | Up to 97% | 620 | Yes | Competitive fixed rates with flexible term options | $2,000 or more |

| Veterans Affairs (VA) | Up to 100% | 580 | No | 100% financing with low fixed rates, no PMI | $2,000 or more |

Step-by-step Guide to Apply for BMO Mortgage

If you’re planning to buy a home in 2025, preparing for the mortgage process in advance can help reduce stress and increase your chances of approval. Below is a step-by-step guide to help you navigate your mortgage journey while making sure you’re in the best position to secure a competitive BMO mortgage rate.

Understand the Full Cost of Homeownership

It’s not just about the home’s price. Your down payment, ideally 20% can impact whether you’ll need to pay Private Mortgage Insurance (PMI) and even influence your BMO mortgage rate. Some BMO programs allow down payments as low as 3%, depending on your financial profile.

Also factor in monthly expenses beyond your mortgage, such as utilities, property taxes, home insurance, and routine maintenance. Creating a realistic monthly budget will prevent surprises down the road.

Tip: Use BMO’s pre-qualification tools to estimate how much house you can afford before you start shopping.

Check and Boost Your Credit Score

Your credit score directly affects the mortgage rate you’ll be offered. A higher score can unlock a lower BMO mortgage rate, saving you thousands over the life of the loan.

Before applying:

-

Check your credit report and correct errors

-

Lower outstanding debts

-

Avoid applying for new loans or credit cards

-

Pay bills on time (automatic payments help!)

You can monitor your credit health using BMO CreditView in the BMO Digital Banking app. If needed, explore BMO’s Credit Builder Loan Program to improve your standing.

Know Your Debt-to-Income Ratio (DTI)

Lenders use your DTI ratio to determine how much of your monthly income is spent on debt. A lower DTI generally means better mortgage terms and a stronger shot at a low BMO mortgage rate.

Gather Your Documentation

Having the right paperwork ready speeds up approval and keeps your BMO mortgage rate lock intact. Key documents include:

-

Government-issued ID and SSN

-

2 years of W-2s or pay stubs

-

Tax returns (2 years)

-

2–3 months of bank statements

-

Proof of other income (rental, pension, etc.)

-

Debt details: student loans, auto loans, credit cards

-

Landlord letter (if applicable)

-

Gift letter (if any family helps with the down payment)

Good to know: You can submit many of these online through BMO’s secure portals.

Start Saving for Closing Costs

On top of your down payment, expect to pay 3%–6% of the home price in closing costs, which may include:

-

Property appraisal and title insurance

-

Legal fees and home inspection

-

Property tax adjustments and transfer fees

-

Fire/property insurance premiums

You’ll receive a Loan Estimate within 3 business days of your mortgage application, and a Closing Disclosure at least 3 days before your official closing. While some closing costs can be rolled into your loan, keep in mind it may slightly raise your BMO mortgage rate or monthly payment total.

Planning ahead is the best way to get approved quickly and lock in a favorable BMO mortgage rate. Each step brings you closer to homeownership with confidence.

In 2025, BMO mortgage rates offer a strong mix of competitive pricing, flexible options, and borrower-friendly features. Whether you’re buying your first home or refinancing, BMO provides the tools and support to help you secure a rate that fits your goals. With added remarkable features, BMO remains a trusted choice for smart home financing.