Your dream home starts with the right financing, and a First Horizon home loan could be your key to unlocking it.

Whether you’re looking to settle down, upgrade, or invest in new construction, First Horizon provides a wide range of mortgage options to fit your goals. This article will guide you through the full journey, covering loan choices, refinancing, tools, and tips to help you take the next big step in life.

What Is a First Horizon Home Loan?

A First Horizon home loan is a mortgage product offered by First Horizon Bank that helps you finance or refinance a home. These loans are designed for people at different stages of the homeownership journey, whether you’re buying your first house, upgrading, refinancing to save money, building a new home, or borrowing against the value of your current home.

Depending on your needs, you can choose from:

- Home purchase loans to buy a property

- Refinance loans to change your interest rate or loan terms

- Construction loans to build your dream home from the ground up

- First Horizon home equity loans or HELOCs (Home Equity Lines of Credit) to borrow against the equity in your existing home for renovations, education costs, or other large expenses

First Horizon offers both fixed-rate and adjustable-rate mortgages (ARMs). With a fixed-rate loan, your monthly payment stays the same for the life of the loan. With an ARM, your interest rate starts lower but may adjust over time. Some of their programs also offer low down payment options and may not require private mortgage insurance (PMI), which can help you save on monthly costs.

First Horizon Home Loan Options

First Horizon provides a comprehensive range of home finance options designed to satisfy different client requirements:

- Purchase Loans: These are traditional mortgages used to buy a home. You can choose your term length, rate type, and down payment amount depending on your budget and qualifications.

- Refinance Loans: If you already own a home, you can refinance your existing loan to lower your interest rate, reduce your monthly payment, or shorten the term of your mortgage. Refinancing may also allow you to switch from an adjustable rate to a fixed one for more stability.

- Construction Loans: If you plan to build a new home rather than buy one that’s already built, First Horizon offers construction loans that provide funding through each phase of the building process. These loans are typically interest-only during construction and then convert to a traditional mortgage once the home is complete.

- Home Equity Loans and HELOCs: These First Horizon home loan products allow you to borrow money based on the equity you’ve built in your home. They are great options for large expenses such as home repairs, college tuition, or medical bills.

- Private Client / Medical Professional Loans: For high-income professionals, such as doctors, dentists, and other qualified individuals, First Horizon offers special mortgage programs with exclusive benefits. These may include 100% financing (no down payment), no PMI, and customized repayment terms. These loans are designed to help professionals with significant earning potential secure homes even if they have limited savings or are early in their careers.

Types of First Horizon Mortgages

When it comes to financing your home, First Horizon offers a variety of mortgage options designed to match different budgets, lifestyles, and homeownership goals:

Conventional Fixed-Rate Mortgage

A fixed-rate mortgage means your interest rate stays the same for the life of the loan. You’ll have stable monthly payments that are easy to plan for.

- Down payment: 20% to avoid private mortgage insurance (PMI), or at least 5% with PMI.

- Best for: Buyers who plan to stay in their home for many years and want long-term predictability.

Adjustable-Rate Mortgage (ARM)

An adjustable-rate mortgage starts with a lower interest rate for a set number of years. After that period, the rate adjusts based on the current market conditions. The main benefit of this First Horizon home loan is the lower monthly payments in the early years, which can save you money upfront.

- Down payment: Typically 5% to 20%.

- Best for: Buyers who expect to move or refinance within a few years.

FHA Loans

Backed by the Federal Housing Administration, this loan has easier credit requirements. They come with more flexible approval guidelines and require a smaller down payment. This makes it easier for many first-time buyers to qualify, even if their credit isn’t perfect.

- Down payment: As little as 3.5%.

- Best for: First-time buyers or those with limited credit history.

VA Loans

VA loans are designed for U.S. veterans, active-duty service members, and eligible members of the military and their families.

One of the biggest benefits is that no down payment is required, and you don’t have to pay PMI. VA loans also offer competitive interest rates that can save you money over time.

To qualify, you’ll need a Certificate of Eligibility (COE) from the VA. If you’ve served in the military, this First Horizon home loan could be your most cost-effective path to homeownership.

USDA Loans

A USDA loan is backed by the U.S. Department of Agriculture and is specifically designed for buyers in rural and some suburban areas.

This loan comes with no down payment requirement and usually offers lower interest rates. To qualify, your income must fall within certain limits, and the property must be located in a USDA-eligible area.

If you’re planning to buy a home in a rural or semi-rural community, this could be an excellent low-cost financing solution.

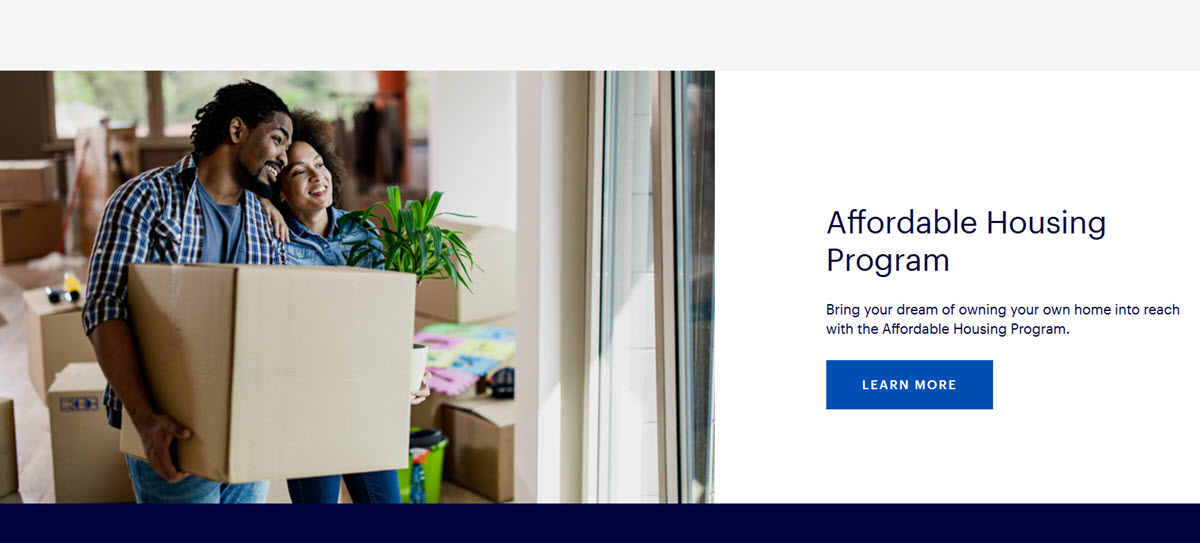

Affordable Housing Program

First Horizon also offers a special Affordable Housing Program for low-to-moderate income borrowers. This program is meant to help more people become homeowners, even if they don’t have a large down payment saved.

- Minimum down payment: As low as $500.

- Best for: Budget-conscious buyers who need a more affordable way to own a home.

Refinancing with First Horizon

Refinancing through First Horizon can help improve your finances. Whether you want to save money, shorten your loan term, or unlock your home’s equity, First Horizon has refinancing options that can make it easier.

Benefits of Refinancing

- Lower your monthly mortgage payment

- Get a better interest rate

- Switch to a shorter loan term (like 15 years)

- Take out cash using your home equity for renovations, tuition, or debt consolidation

Refinance Loan Options

Here are some common types of refinance loans First Horizon offers:

- Rate-and-Term Refinance: Change your interest rate or the length of your loan

- Cash-Out Refinance: Tap into your home’s equity and receive cash

- FHA/VA/USDA Streamline Refinance: A faster First Horizon home loan option for those who already have government-backed loans

These refinancing options are designed to meet different financial goals, whether you’re looking to save money or gain more flexibility.

Documents Needed to Refinance

To get started, you’ll need to gather a few documents. Here’s what most borrowers should prepare:

- Proof of income (like pay stubs or W‑2s)

- Recent tax returns

- Credit report

- Details of your current mortgage

Most refinance applications close within 30 to 45 days, depending on your situation and how quickly documents are submitted.

Construction Loans

If you’re ready to build your dream home from the ground up, the First Horizon home loan program offers flexible construction-to-permanent financing:

- Single-close loan: Instead of getting two separate loans, one for building and another for your mortgage, you’ll only need one. This is called a single-close loan, which saves you both time and money.

- Interest-only payments: During construction, you’ll make interest-only payments, which help reduce your expenses while the home is being built. After that, the financing will immediately change into a regular long-term mortgage after construction is finished. No second closing needed.

- Up to 80% financing: First Horizon can finance up to 80% of your construction costs, and their team works with you to offer loan terms that match your specific project timeline and budget. Whether you’re working with a builder or managing the construction yourself, their experienced loan specialists are there every step of the way.

First Horizon Home Equity Line of Credit (HELOC)

If you’ve built up equity in your home, First Horizon makes it easy to turn that value into flexible spending power with a Home Equity Line of Credit (HELOC). Whether you’re upgrading your kitchen, consolidating debt, or covering a big expense, this revolving credit line gives you control over when and how you borrow.

Why Choose First Horizon’s HELOC?

Here’s what makes First Horizon’s HELOC stand out:

- Lower Interest Rates: Rates of First Horizon HELOC products are usually less expensive than the rates of personal loans or credit cards.

- Interest-Only Payments During Draw Period: Keep payments low while managing other expenses.

- Flexible Access: Use online banking, checks, or even link to your First Horizon checking account for overdraft protection.

- Reusable Credit Line: Pay it down and borrow again anytime during the draw period.

- Dedicated Loan Specialists: Personalized guidance throughout the process.

How to Qualify

To be approved for a HELOC with First Horizon, you’ll generally need:

- Sufficient home equity (typically at least 15%–20% equity remaining)

- A good credit score

- A stable income and manageable debt-to-income ratio

- Proper documentation (income proof, tax returns, mortgage note, etc.)

Your loan officer will walk you through the details and help you determine the right line amount based on your financial goals.

A Home Equity Line of Credit (HELOC) gives you flexible access to funds whenever you need them, making it a smart option for many situations. You can use this First Horizon home loan to pay for home renovations or repairs, cover education expenses like tuition, or consolidate high-interest debt into one manageable payment. It’s also helpful for unexpected medical bills, emergency costs, or big one-time purchases you’ve been planning. With a HELOC, you’re in control of how and when to use your money.

Who Can Qualify for a First Horizon Home Loan?

Getting approved for a First Horizon home loan is straightforward if you meet a few key requirements. The bank reviews your full financial picture to make sure you’re able to repay the loan. Here’s what most borrowers need:

- Good Credit Score: While First Horizon doesn’t list a fixed minimum, most programs prefer a score of at least 620 or higher. Some specialized loans may accept slightly lower scores with strong income or assets.

- Stable Income and Employment: You must show proof of income. This can include recent pay stubs, W‑2s, tax returns, or bank statements.

- Reasonable Debt-to-Income Ratio (DTI): Your DTI compares your monthly debts to your gross income. Most home loan programs at First Horizon accept borrowers with a DTI below 43%, but the lower, the better. A lower DTI shows you aren’t overextended financially.

- Home Appraisal That Matches Loan Value: Before approval, First Horizon requires a home appraisal. This helps ensure that the property is worth the amount you’re borrowing. You may need to renegotiate the purchase price or modify your loan amount if the home’s value turns out to be less than anticipated.

- Special Requirements for Medical or High-Earning Professionals: If you’re a doctor, dentist, or other high-earning professional, this bank offers special First Horizon pharmacist home loan programs just for you. These often include:

- Up to 100% financing (no down payment)

- No private mortgage insurance (PMI)

- Flexible credit and income guidelines

First Horizon Home Loan Application Process

Applying for a First Horizon home loan is easier than you might think. Here’s a simple breakdown of how to get started with your First Horizon Bank home loan:

- Use the calculators: Before choosing a loan, play around with First Horizon’s online calculators. They’ll give you a clearer picture of what you can afford and what your payments might look like.

- Talk to a loan officer: Reach out online or visit a local branch. A loan expert will explain your options and guide you through the next steps.

- Choose the right loan option: Select a loan that matches your budget, goals, and lifestyle. Whether you’re buying, building, or refinancing, there’s a solution for everyone.

- Get prequalified: Prequalification shows sellers that you’re a serious buyer. It also gives you a more realistic budget so you can shop with confidence.

- Gather your documents: To apply for a First Horizon home loan, you’ll need some basic paperwork:

- Proof of income (like pay stubs or tax returns)

- Bank statements

- Photo ID

- Employment history

- Information about any debts or assets

- Submit your application: Provide all needed documents so the bank can verify your income, assets, debts, and overall creditworthiness.

- Review your loan estimate: Within three days, you’ll get a Loan Estimate showing your rate, monthly payments, and closing costs.

- Lock your rate: If you’re happy with the terms, you can lock your interest rate to protect it from market changes.

- Appraisal and underwriting: The bank orders a home appraisal and reviews your full file to ensure everything checks out.

- Close your loan: When you’re approved, you’ll sign the final paperwork, pay any closing costs, and officially become a homeowner or start construction on your dream home!

Rates, Fees, and Mortgage Insurance

When applying for a mortgage with First Horizon, it’s important to understand the costs involved. The total cost of your First Horizon home loan depends on your financial profile, the type of loan you choose, and market interest rates at the time of application.

First Horizon Home Loan Rates

The table below gives you a quick look at average First Horizon mortgage rates for 2025 so you can compare your options more easily:

| Loan Type | Average Rate (2025) | Best For |

|---|---|---|

| 30-Year Fixed Mortgage | ~7.35% | Long-term buyers seeking stability |

| 30-Year Refinance | ~6.69% | Homeowners wanting better terms |

| 15-Year Fixed Mortgage | ~6.21% | Buyers who want to pay off faster |

| VA Purchase Loan | ~6.30% | Eligible military personnel |

| FHA Loan (30-Year) | ~6.50% – 6.90% (varies) | Buyers with lower credit or low down payment |

Note: All rates are approximate and based on 2025 national averages for First Horizon. Your exact rate may vary based on your credit profile, loan type, and property location. Always request a Loan Estimate before committing.

First Horizon Mortgage Fees & Insurance

Besides the mortgage rates, you will also need to consider extra costs like closing fees and mortgage insurance. These costs can impact your budget, especially if you’re a first-time buyer. Here’s a simple breakdown of the common fees and insurance costs you might encounter with a First Horizon home loan:

| Fee / Cost | Details |

|---|---|

| Application Fee | $0 (free to apply online) |

| Appraisal Fee | Paid separately, non-refundable |

| Closing Costs | Average ~$6,428 for $400K loan (2%–5% of loan amount) |

| PMI (Private Mortgage Insurance) | Required for conventional loans <20% down; removable at 78% LTV |

| MIP (Mortgage Insurance Premium) | Required for all FHA loans; 1.75% upfront + monthly premium |

| VA Loan Insurance | No mortgage insurance required |

| USDA Loan Insurance | No traditional PMI; guarantee fees may apply |

Pros and Cons of First Horizon Home Loans

Before choosing a lender, it’s important to weigh both the benefits and the drawbacks. Here’s what you should know about First Horizon’s home loan offerings:

Pros:

- Offers a wide range of mortgage types, including First Horizon home equity line of credit, conventional, VA, FHA, USDA, and jumbo loans.

- Special Affordable Housing option with low or no private mortgage insurance (PMI).

- First Horizon physician mortgage loan with 100% financing and no PMI

- Access to physical branches across 12 states, mainly in the Southeast.

- A great choice if you already have a personal banking relationship with First Horizon.

- Generally lower closing costs compared to many other lenders.

Cons:

- Does not provide a full online application process, most steps are handled offline.

- Interest rates and fee details are not published clearly on the website.

- Some borrowers have reported issues after closing, such as payment processing delays, limited customer support, or difficulty making loan changes.

First Horizon Home Loan FAQs

How much down payment do I need for a First Horizon mortgage?

- It depends on the loan type. Conventional loans typically require 5%–20%, FHA loans require at least 3.5%, and VA or USDA loans often require no down payment.

Does First Horizon charge application fees?

- No, First Horizon does not charge a fee to apply for a mortgage online. However, you may still need to pay for third-party services like appraisals.

Is mortgage insurance required with a First Horizon Bank home loan?

- Yes, if your down payment is less than 20% on a conventional loan. FHA loans also require mortgage insurance. VA loans do not.

How long does it take to get approved for a home loan at First Horizon?

- Approval usually takes anywhere from a few days to a few weeks, depending on your loan type and how quickly you submit the required documents.

Getting a mortgage doesn’t have to be confusing or overwhelming. First Horizon home loan products offer flexible terms, competitive rates, and expert support to help you reach your homeownership goals. Whether you’re dreaming of a quiet starter home or planning to build from the ground up, First Horizon is ready to help make it real.